Best Cash Back Credit Card

Having scan through the majority of credit card cash rebates, I had reduced to 3 best credit card that truely gave you good cash back rebates and are simple to understand and used.

These credit card does not break your spending into different categories and there is no minimum amount before you can get your cash back.

These credit card are chosen as they also include the minimum spending into your cash back.

1. UOB One Card (Visa)

Criteria to fulfill.

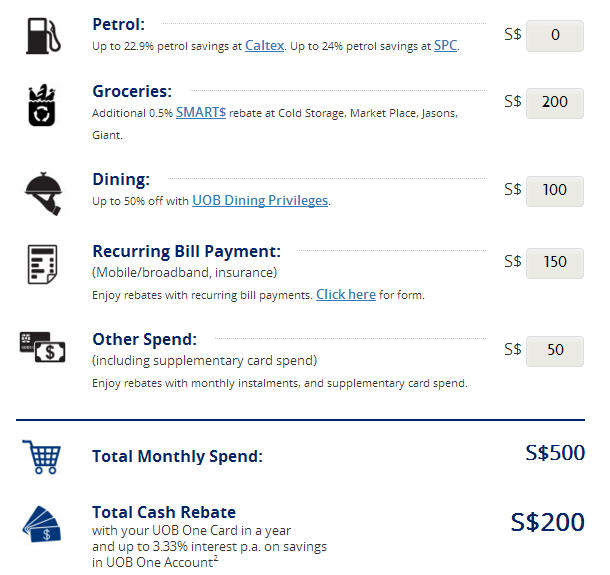

Monthly spend of 500 for 3 months = 50 cash back (3.33 %)

Monthly spend of 1000 for 3 months = 100 cash back (3.33 %)

Monthly spend of 2000 for 3 months = 300 cash back (5%)

Updates - Recently they make changes where these transaction are not included as part of the spending:

- Any Government payment - Town Council, Singapore Police (learning driving), Singapore School (NUS, NTU, SIT, SMU), Dental treatment at Ng Teng Fong or any Hospital.

- Any kind of monthly installment.

- Charity and Temple.

Now, for the average Singaporean, this is the best card that can save you 50 SGD every quarter. Many families have telco bills of at least 100-200 SGD monthly for a small family of 4. So, you only need to spend the balance of around 350 or less on your UOB One credit card.

For those who spending are 1000 SGD monthly, you save 100 SGD every quarter.

First determine your monthly spending amount. Then target your spending range 500, 1000, or 2000 SGD.

Once you hit your monthly target spending range, use another card like America Express True Cashback or Standard Chartered Manhattan.

How the 3rd month works:

500 Spending - 50 cash rebates = 450 SGD (on the 3rd month where your cash rebates was deducted you will failed the last quarter fulfillment).

550 Spending - 50 cash rebates = 500 SGD (you fulfill the cash rebates deduction month).

I used the UOB One cash rebates calculator and you can see that the monthly spend of 500 SGD is quite easy to hit as it include the recurring bill payment.

Take note that recurring bill does not include installment plan with free interest.

2. American Express True Cashback Card / Standard Charted Unlimited Cashback Credit Card

For those who hate to keep track of things, then this is a no-brainable card. Nothing to keep track and you get 1.5% cash rebates every month. However, if compared with the UOB One card for 3 months (50 - 22.50 = 27.50). If you don't mind the differences then this no-brainable card is the best.

If possible, apply for your American Express True Cashback or Standard Charted Unlimited Cashback Credit Card when you have some BIG amounts payment like booking a tour.

American Express True Cashback give new members a bonus of 3% cash back for the FIRST 6 months up to 5,000 SGD spend. This gave you a saving of 150 SGD cash rebates.

Once the 3 months bonus period is up, you will still earn a fixed rate of 1.5% cash rebates with NO CAP.

3. Standard Chartered Manhattan Card (Master)

| 1-999 | you get cash rebates of 0.5% |

| 1000-2999 | you get cash rebates of 1% |

| 3000 and above | you get cash rebates of 3% |

From the above cash rebates percentage, Manhattan card is useful when you have BIG amount spending that is 3000 and above as you can get cash rebates up to a maximum of 200 SGD per quarter which requires a spending of 6670 SGD if you wish to maximize it.

---

Other Cash Back Credit Card

Nowadays, majority of customers prefer Cash Back credit card and non-cash back credit card are seeing lesser sign-up.

Required a monthly total spending of S$888 or more before you can get 8% and each category cash back is capped at $25. You only get 0.25% if your spending falls below S$888.

Dining: 8% cash back at all restaurants, cafes, bars worldwide. foodpanda delivery counts too.

Grab rides: 8% cash back on all Grab rides.

Groceries: 8% cash back at all supermarkets and groceries worldwide. honestbee and RedMart delivery counts too.

Petrol: Up to 20.88% fuel savings at Esso & Shell, and 8% cash back at all other petrol stations worldwide.

My Dislike Reason: Quite

restrictive criteria as they know that many people will spend more on 1

category only and Cash back is withheld

if it falls below S$50.

Criteria to fulfill.

Minimum total spending of S$600 or more capped at S$40 per month. (actually is $60 but the last $20 of 0.3% you should used AMEX or Standard Charted Unlimited Cashback Credit Card which is at 1.5%.

5% cashback on your eligible online purchases and Visa payWave (Apple Pay, Samsung Pay and Android Pay are considered as Visa payWave transactions) purchases and 0.3% cashback on other eligible retail purchases. (Earn up to $720 cashback a year).

However, each category is capped at $20, the last category 0.3% also capped at $20 but don't worry as you will never hit $20 at 0.3%.

- Online Purchases - So amount more that $400 will be excluded.

- Visa PayWave - So amount more that $400 will be excluded.

My Dislike Reason: Quite

restrictive criteria as they know that many people will spend more on 1

category only and Maximum cash back is only

$40 because the last category is only 0.3% which you might well use the

1.5% card from Amex or Standard Chartered Unlimited.

Conclusion

If you have read the fine print, the majority of the credit card does not include the minimum amount spend or set criteria that are different to met unlike the above credit cards. Secondly, the cash rebates are automatically deducted in your next payment once you fulfill your spending without any manual redemption.

Personally, UOB One is my main credit card I used for all payment. Once I hit my targeted monthly spending, I will use American Express True Cashback card (1.5%) or Standard Charted Unlimited Cashback Credit Card (1.5%).